Demand for Craft Beer in United Kingdom Remains Strong

Story by:

Editorial Dept.

Story by:

Editorial Dept.

According to BMI Research (Business Monitor International, a unit of Fitch Group), the “U.K.’s wealthy consumer base and growing sophistication in tastes offers significant growth prospects for premium alcoholic drink categories, including craft beer.”

Heineken, in particular, is looking to make headway into the craft beer sphere after its competitors, AB InBev, SABMiller and others, have acquired various craft breweries over the years.

The full report from BMI Research regarding the U.K.’s beer numbers is below.

Company Trend Analysis – UK Craft Beer Demand Will Not Falter Anytime Soon

26 Jun 2018 United Kingdom Food & Drink Heineken

BMI View: UK’s wealthy consumer base and growing sophistication in tastes offers significant growth prospects for premium alcoholic drink categories, including beer. Looking to tap into this market, Heineken has acquired a minority stake in London-based craft brewer Beavertown Brewery, signalling the former’s desire to focus and strengthen its craft beer portfolio. However, we caution that Heineken will need to invest further in craft beer in order to keep up with competition and gain greater exposure to this space.

Heineken has acquired a minority stake in London’s Beavertown Brewery in the latest move by an alcoholic drink major to expand its presence in the craft beer market. Heineken will provide a GBP40mn cash injection to help Beavertown Brewery build a new production facility approximately ten times the size of its current one, which will enable the brand to not just expand in the UK but overseas as well. Beavertown will also be able to gain access to Heineken’s 2,900 pub network in the UK, having completed the acquisition of pub operator Punch Taverns in August 2017. Heineken also announced in June 2018 that it would be upgrading 500 of its UK pubs as part of a GBP44mn investment.

Slow To The Game

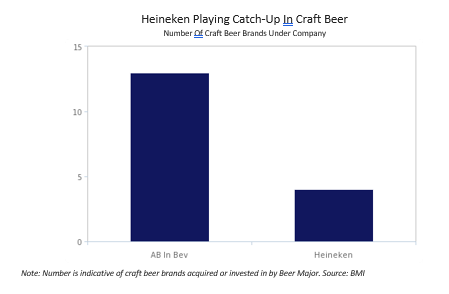

The minority stake in Beavertown Brewery will help Heineken expand its craft product portfolio which includes US-based Lagunitas, which Heineken acquired fully in 2017, and French brands Affligem and Mort Subite. However, we note that Heineken’s craft beer portfolio remains relatively small in comparison to its biggest rival AB InBev, with the former slower to tap into the craft beer movement. Between 2011 and 2016, AB InBev invested in 9 craft breweries and in 2017 added a further 4 craft breweries to their portfolio: Boxing Cat in China, Wicked Weed in the US and 4 Pines and Pirate Life in Australia.

Meanwhile, Heineken’s craft beer portfolio is much smaller with just three brands and even launching its own craft beer brand under the Maltsmiths banner in March 2017 (see ‘Challenges Abound For Heineken’s Craft Brand’, May 8 2017). We have previously highlighted the challenges facing Heineken’s own craft beer brand and that it is wiser to acquire or take a stake in existing microbrewery and remain a silent partner, allowing the craft business to essentially govern themselves, with minimum input from the parent company. This ensures that the authenticity of the brand is maintained, which consumers continue to look out for in their choice of craft beers.

Heineken Playing Catch-Up In Craft Beer

Number Of Craft Beer Brands Under Company

Note: Number is indicative of craft beer brands acquired or invested in by Beer Major. Source: BMI

According to Heineken’s global financial results for 2017, its craft and variety category grew by double digits, driven by Affligem and Mort Subite in France and Lagunitas in the UK and US. Craft beer, along with its low/no-alcohol (LNA) category, were key in supporting positive 4.5% growth in overall beer volumes in FY17. In line with consumer trends, we expect Heineken to continue focusing on strengthening its craft beer portfolio both in the UK and globally from 2018 onwards.

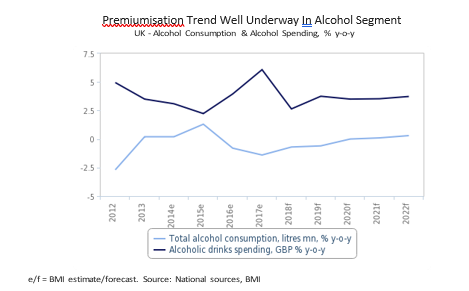

Premiumisation Well Underway In The UK

There is a clear outperformance in the value growth of alcohol spending in the UK in comparison to volume growth, with alcoholic drinks spending projected to grow by an average 3.4% annually between 2018 and 2022 in local currency terms, reaching total spending of GBP24.2bn in 2022, up from GBP21.0bn in 2018. By comparison, alcohol consumption in litres will decline by 0.2% annually over the same period. We note that this premiumisation trend, of consumers spending on higher-priced alcohol drink categories perceived to be more niche and of a better quality, to have long been apparent in the alcoholic drinks market with this trend evident in the UK since 2012.

Premiumisation Trend Well Underway In Alcohol Segment

This premiumisation trend in the UK beer market is driven by the generally high disposable income levels of consumers. Over 94.5% of households in the UK have disposable income of USD25,000-plus – the indicator we use to indicate the ability of households to begin to purchase premium alcohol – and this is expected to grow further to 96.3% of total households by the end of our forecast period in 2022. Meanwhile, the upper-income segment (household disposable income of USD75,000 and above) is also forecast to see robust growth with 43.5% of total households falling into this segment by 2022, up from 33.8% in 2018.

We note that craft beer such as those produced by Beavertown Brewery will mostly appeal to millennials and young working adults (20-39 years old) who are in the age group that is keen to try innovative and authentic brands and are heavily influenced by social media trends. Beavertown Brewery’s brightly coloured cartooned beer cans with interesting and unique names such a Gamma Ray American pale ale and Neck Oil IPA will likely appeal to millennials, the key target audience. This is particularly the case in Western European and North American markets where young adult consumers have greater exposure to the bar culture and also the incomes necessary to support the higher cost of craft beer.

Backlash From Craft Beer Community

We have already seen considerable backlash as a result of Beavertown Brewery’s deal with Heineken, with various craft beer companies such as Cloudwater Brew, Brew Dog and Hop Burns & Black pulling out of the Beavertown Extravaganza Festival scheduled to take place in September 2018. This is likely the result of the discontentment among some consumers and market peers over Beavertown ‘selling out’ to a beer major.

Although Beavertown may lose some of its core support base, we believe this is outweighed by the ability to use Heineken’s expertise to expand into new markets, boost production and distribution outlets. In particular, we note that Beavertown is likely to want to expand its reach into other developed markets in Western Europe and North America, where a similar premiumisation trend is well underway although in a market where competition is not as fierce.

Canada And Germany Next On The Radar?

We have previously noted a similar craft beer trend in Australia, with UK craft brewer BrewDog entering the market (see ‘Craft Beer Outlook In Australia Continues To Soar’, February 19). Besides Australia, we point out Germany and Canada as markets where this premiumisation trend is well underway and presents a favourable market for Beavertown to expand into. Alcohol spending in Germany and Canada will grow by an average of 2.4% and 3.7% annually between 2018 and 2022, while alcohol consumption will be much lower at -0.3% and 1.2% respectively over the same period.

Comments 0

No Readers' Pick yet.