2026 Beer and Beverage Trends

Story by:

Jim Dykstra

Story by:

Jim Dykstra

In the beer land, the only constant is change. Things undoubtedly changed in 2025. The ranks of craft beer brands are thinning, and in their stead come hordes of alternative drinks – some alcoholic, some psychoactive, and some non-alcoholic. So too are the ranks of craft drinkers. They are aging, ailing, or simply coming into adulthood with minimal interest in what their parents and uncles drink. Much of Gen Z shies away from drinking, preferring vapes, THC, or will rely on the simple terror of genuine social interaction every once in a blue moon.

With a snapshot of the numbers, along with a survey of craft-interested consumers, here’s what is changing, staying the same, and showing promise between 2025 and 2026.

Beer Sales in 2025

First things first: beer as a category is continuing its downward trend, which shouldn’t be a surprise. Total sales are down 3 percent this year, which is a drop of nearly $2 billion, for a total of $37.8 billion annually. Seltzer and Craft are down more than 4 percent, and Domestic Premium is down most of all, over 6 percent. Three segments are actually up. Domestic Super Premium and Cider saw modest growth, and Non-Alcoholic (NA) products had another meteoric year, growing 22.3 percent, for total dollar sales of more than $90 million. Athletic Brewing, by this count, is now a billion dollar brand. The rest of beer sales are looking a bit… tired.

A Year of Fatigue

When excitement wears off, what remains? Fatigue. Without an excess of energy, one’s preference shifts to straightforward over flowery and “well-attenuated” rather than “cloying”. It’s true for communication, and it’s true for what we consume.

Consumers are fatigued by self-indulgent names, overhype, overstimulation, overhopped beer… No-BS lagers have shifted to center stage. The decadence of craft beer’s youth melts into the refined wisdom of maturity.

With maturity comes a reckoning – can I afford the resource expenditure of time, money, and energy? Can I drink all night and uphold responsibility? Can I buy a 4-pack at a $20 price point? It’s not sustainable, without consequences, and therefore, faithful craft drinkers must be increasingly judicious. So too must producers, as resources are equally scarce on their end.

Brewers too, are reckoning with the end of their experimental Wild West, Woodstock, Roaring 20s era. Dumping cocoa puffs in a stout recipe isn’t going to work anymore. So, the wheat is separating from the chaff. Specialty brewers who nail the technical aspects of a refined style stand a better chance than slingers of peanut butter and jelly brews. This will appear to the 32 percent of consumers who are drinking less alcohol because of “health reasons.”

Functional Drinking and Where Beer Wins

That’s right, almost a third of consumers are concerned about beer bellies. It’s a symptom of more options (low calorie seltzers), aforementioned fatigue, and the pressure of the increasingly superficial, aesthetically-motivated world of appearances which we swim in. Every step-counting watch, every photo shared, pushes us toward valuing looks and quantifiable returns, and often, forgetting the magic that comes when quality is prioritized above quantifiables.

Some might call this “left-brained drinking” – where one’s decision-making comes primarily from abstract rationales rather than feeling. Beer wins on feeling. It’s liquid comfort food. It’s pancakes and maple syrup around a fire with your closest friends. Beer wins on intangible aspects of human experience.

Beer captures the “old world charm” and “most quaffable beverage” categories. Not a huge wellspring of sales, but something to lean on. While one can get drunk with less calories by drinking seltzer, it can’t compete with “cracking a cold one with the boys,” or “toasting your oldest friend’s promotion after a year apart.” Beer is nice for generational bonding moments.

Marketing-wise, beer’s appeal is in celebrating the moment. Don’t underestimate the commemorative aspect of beer. Commemoration is living in the present, something drinking is all about. Functional drinking is essentially trying to steal fire or, having the cake without actually eating it.

Here again is where breweries and pubs can corner an intangible market: they are still, as they always have been, public houses. Places for gathering and commiserating. Places for discourse that are sorely needed and disappearing in America, where there are no longer “third spaces.” No one discusses plans to become an independent nation while sipping Truly. And you don’t generally take your kids to an afternoon at the distillery, if for no other reason that liquor is not great for prolonged drinking. It’s concentrated. Again, it’s pubs and breweries that are best situated for day-to-day human leisure, conversation, and celebration of life.

Brewers might find success in prioritizing their communities, supporting growth and celebration of those who will in turn support the brewery for its vital role in the community. Community-minded folks are typically less concerned with quantifiables, because there’s not often a direct quantifiable return for helping one’s neighbor.

The Non-Alcoholic Surge

Of the top 100 beer brands, eight are NA. Three are from Athletic Brewing Co., namely Run Wild IPA, Upside Dawn Golden Ale and Free Wave Hazy IPA, all of which are ahead of Busch NA. Of the three Athletic varieties, Run Wild boasts the strongest sales. Corona NA is roughly equivalent to Run Wild’s sales at $25 million.

Slightly ahead at $28 million each are Budweiser Zero and Michelob Ultra Zero, the latter of which debuted this year, poaching sales from Bud Zero, and promising significant growth for 2026, as one of the most beloved “Functional Drinking” brands.

Topping the charts is Heineken 0.0, which saw a strong increase to $47 million in sales this year. Worth noting, however, is that combined, Athletic Brewing’s top three sellers would surpass Heineken in sales, allowing for the argument that Athletic is the true king of NA beer. After all, it’s craft. And lastly, a solitary trumpet dirge for O’Douls, which no longer featured as a top 100 brand. Unfortunately, it’s going to need a bit of a miracle to compete in terms of marketing with any of the NA’s listed above.

All told, we can safely predict another few years of steady increase for non-alcoholic beer, at least. Time will tell how far it will rise, but as a healthy alternative, it’s got legs. More than two legs. It’s got entire months that bolster sales: Sober October, Dry January. It’s got an entire state of mind behind it in functional drinking. It has relatively few direct competitors.

Best of all, it likely rings more interest to craft beer than it takes away in market share as an indirect competitor. To that end, more than 90 percent of Athletic drinkers do enjoy alcoholic brews.

Can brewers overcome the logistical and technical hurdles to incorporate NA beers into their roster? Sure, it may not be easy, but it would provide a much firmer base for those who hope to be around for another five years. Or perhaps we’ll see an NA craft competitor emerge. It’s hard to imagine one coming close to the monopoly that Athletic has developed as the first to market. Marketing is something Athletic has done exceedingly well.

Packaging and Branding

Not one of craft’s 22,094 brands is identical, so each must find a way to stand out. As such, there’s been a branding arms race trending towards wacky, zany, whimsical, mustachioed pennyfarthing riders and 90s Nickelodeon SPLAT-type fonts. As that has become the norm, what can one do in 2026? Breathe, simplify. Own the 6-pack’s shelf space like a mini billboard with recognizable, iconic font that implies the beer speaks for itself.

Consider also logo placement, ensuring it’s identifiable. The iconic Left Hand logo comes to mind. Without overwhelming the eyes, see if there’s a “spirit animal” or associated image which can subconsciously enhance brand recognition and help potential drinkers think of refreshment when they see your beer.

Without looking it up, can you remember what Bell’s Two Hearted looks like? A simple, bold font, which stands out without overstatement? What about the simplistic logo? What about the image? It’s a frickin’ salmon. But that one salmon means something.

There is no formula, or one-size-fits-all solution to branding. But consistency and balance between eye-catching and simplicity are reliable benchmarks. Go too far and you begin diluting the potency of your branding.

Brand Equity

For all of Bell’s fine packages, they’ve also gambled on brand equity. Two Hearted is beloved, as is the more polarizing Hopslam. Now we’ve got Tropical Hopslam and Hazy Hearted, Cold Hearted, A Change of Heart. These will sell, initially. But will they last? To what degree will they siphon sales away from Two Hearted? Will Two Hearted move closer to a separate brand entirely, à la Voodoo Ranger? Presumably, they’ve done the research, but any brand which spins off beers from a successful brand runs the risk of shooting itself in the foot.

Two Hearted is secure enough as a brand to take the risk, but for the average IPA brand, one should first ask, “Have I perfected the original?” and “Is this truly a beloved beer?” If you don’t think people would give it a state funeral if it disappeared, it’s probably best to keep things simple.

Sadly, if Marvel movies are any indication, experimental risks are hard to come by these days. It begs the question, how do you take risks in the era of intellectual property Groundhog Day?

Gas Stations and Contract Brews: Lifelines for Mid-Sized Craft

Gone are the days of 7 a.m. lines for bombers, but the era of construction workers buying 19-ounce cans from gas stations has never been stronger. Some call a couple of high-ABV hazy stovepipes “the new malt liquor,” and they’re right. This format of craft is essentially functioning as a premium alternative to malt liquor, providing a more uplifting drinking facade for the buyer who might otherwise grab a couple Colt 45s.

They’re quick, easy, and unlike most craft, still pretty affordable. Generally, you can get a 2 for $4 or $5 deal. They’re a no-brainer, which itself is an antidote to choice fatigue. As we’ve said for a few years now, the savvy craft brewer could explore ways to tailor their products for sale from gas station vendors, which also crank out obscene sales for michelada and Clamato-style beverages, beloved by the Hispanic drinking community which often hits the local bodega after work.

Another interesting development on this front comes from QuikTrip, which has recently revived a house brand, “Quittin Time.” It’s right in the name. People hit the gas station on the way home from a day at the office, or the construction site.

Contract brewed by Tulsa-based Marshall Brewing Co., the beer saw initial release for the Oklahoma market in January of 2025. As of October, the Light Lager brand has expanded to other states like Kansas and Georgia. They’re onto something.

On that note… Have you tried Piggly Wiggly beer yet? It may sound crazy, but it’s real craft beer, with recipes (supposedly) formulated from the ground up by Sheboygan’s 3 Sheeps Brewing. From 3 Sheeps comes three pigs: An Amber, a Pilsner, and a Lager. Classic, simple, with nice packaging. Not trying to be anything it’s not. A solid example for beer in 2025.

Brewers could solicit these sorts of brand partnerships as a viable alternative to relying on more traditional sales channels.

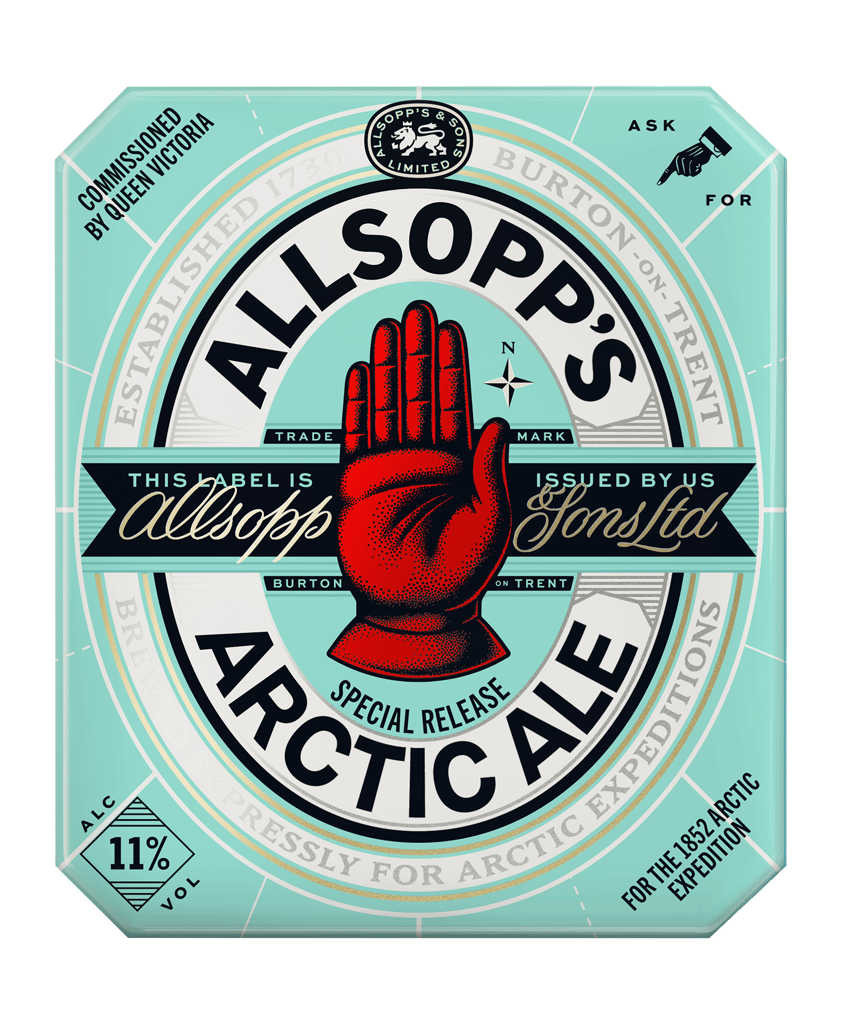

Historical Beers: Old Becomes New

Here’s an interesting way to bring attention and authenticity to a brand. A while back, Dougal Gunn Sharp, founder of Innis & Gunn purchased a 150-year-old bottle of Allsopp’s Arctic Ale found sitting in a garage for £3,000, originally brewed for Sir George Nares’s pioneering 1875 arctic expedition.

Now, he’s cracking it open to seed a new limited-edition collaboration with a revived Allsopp’s Brewery following the original recipe. Interestingly, this is a beer with legitimate functional use, designed as it was to provide sustenance for sailors enduring temperatures as low as -400C.

Weighing in around 9% ABV, it was strong and nutrient rich, with lots of unfermentable sugars that could resist freezing, plus “six times the calorie content of conventional beer.” Records from the time describe the Arctic ale as dark brown and so thick it had to be lifted from the brewing copper in buckets. That’s a far cry from an average drinking experience, pointing to another to differentiate oneself in an overcrowded market.

Then again, this line of thought is not new, even in modern times. Dogfish Head has made it a staple of production since 1999 with its “Ancient Ales” line. You may recall Midas Touch, “based on molecular evidence found in a Turkish tomb believed to have belonged to King Midas,” and “brewed with honey, white Muscat grapes, and saffron.”

The key takeaway is that brewers hoping to stand out in such a saturated space may have to build a new niche, rather than carve one out in an existing space.

Brave New World of Beer

Last year, informed consumer perception pointed towards more faith in the family friendly brewery over beer-geek models. There’s still a place for both. Brewers are looking backwards and forwards to dream up new ways to keep the public’s waning interest.

Some even tried to build a reputation as “AI breweries”. Anathema as it feels to the human element of beer, breweries like the former Intelligent X in the UK, which fed its AI customer feedback to influence its beer recipes, are riding the techno wave.

Until 2024, Species X Brewing made “Carbon” and “Silicon” brews, the former recipes designed by humans, and the latter tweaked or entirely designed by AI models. Perhaps the most intriguing came from the “Behemoth” model, which spat out a “Baltic porter with 10% ABV and hints of lactose, marshmallows, vanilla, chocolate, coffee and three different types of fruit.” Founder Beau Warren stated at a recent launch event: “I would never even have thought of making a beer like that. It’s absurd.” It is. And to be fair, it certainly sounds unique.

For now, however, the standalone AI brewery remains more of an idea than reality, as both of the aforementioned AI projects are no longer in business.

AB InBev is also leveraging AI in its Leuven facility, where Boston Dynamics’ doglike Spot robot performs 1,800 maintenance checks a week. Perhaps the most understandable application relates to quality assurance, with breweries such as Deschutes or Sugar Creek Brewing Co. in Charlotte using AI to check batches of beer and packaging, respectively.

When sales are dropping, everything counts, and few things count more than quality assurance. While AI is generally off-putting against the backdrop of beer’s profoundly human element, the middle path may be exploring where this sort of technology can genuinely improve the drinker’s experience.

In-Cider Information

Angry Orchard Crisp Apple accounts for the largest segment of U.S. Cider sales, coming in at $118 million of Cider’s total $422 million. As the only Top 100 brand that is a cider, it’s safe to assume that other Angry Orchard styles will account for a significant chunk of sales as well. There then will be a long tail of local brands with modest sales.

What would be interesting to know is how much of these sales for any cider brand are coming from 19-oz cans, rather than 6-packs. Cider has also found a home as a malt beverage alternative, as its sugar content can easily mask a high ABV. Further, for those who are not past the palate adaptation that comes with learning to love the bitterness of beer, cider is a happy medium that dodges the “lesser-than” associations with Malt Beverages and retains a craft veneer. Considering this market is one of only a handful that saw growth, if your taproom is not offering cider, it would be worth considering. In this era of Fatigue, the market dictates what will sell.

Creativity vs. Market Dictation

Our current beer landscape is not ideal for a starry-eyed beer producer. Ultimately, brewers are increasingly catering to what sells rather than what they actually are excited by. While quality of one’s product always has an impact on sales, the market dictates production, and the current market for beer drinking is mostly lighter beer, IPA, and seltzer, with room for a little seasonal flavor.

There is plenty of pride in simply being a brewer. It may be encouraging for beer lovers and producers to recapture a bit of the magic of the past not by what is made and consumed, but by how it is shared.

Craft Styles: On a Lighter Note

Our data tracks 26 craft style segments. The bad news? All but two of them saw a drop in sales. The good news? Wheat Beer and Craft Light Lager are doing alright. Wheat Beer is up 10 percent. Craft Light Lager is up by 15 percent. The silver lining, in terms of craft sales? IPA, which has long accounted for half of craft’s total dollar share, saw the most modest decline in sales of any craft segment, dropping just $7 million in comparison to 2024, whereas the relatively paltry sales of Amber Lager ($48 million) fell by $8 million. All things considered, IPA still had a fine year.

An interesting theme: The darker the beer, generally, the worse it is selling. Conversely, the lighter in color, the better. Functional drinking. Less sugar. Mild flavors.

Stout, Porter, Browns, Red Ales, are all down between 9 and 15 percent. Of these styles, only Stout clocks in above 1 percent of total dollar share. Understandable, considering that beyond IPA, it is a style which enjoys some of the highest name recognition.

How do you split the difference? Try a dark light beer, or Black Lager. Perhaps you recall Negra Modelo, a Top 100 brand with minimal competition. It’s as crisp of a dark beer style as you can find, yet still light on calories and carbs, and significant flavor. Among dark lagers, German Dark Lagers, or Schwarzbiers are seeing a rise amongst the specialty craft brewers who focus on regional styles from across the pond. Köstritzer has earned a lot of fans stateside, for example.

Wheat Beer revels in its title as “most improved” for 2025, having increased its sales by the highest percentage relative to its position in the category. Here we have an approachable, understood style, classic, full-bodied and flavorful, while still registering as “light”. They are easy drinking, and easy to digest. Most would consider it easier to drink a few wheats than a Session IPA of similar ABV.

Beyond Light and Dark

Pilsner didn’t have a bad year. All told, this segment dropped by less than a percent, signaling a pretty stable footing. Pale Ale didn’t fare as well, dropping 5.5 percent, but still fared better in terms of sales stability than most remaining segments.

Belgian Wits deserve a shout out. Despite a 10 percent decrease in dollar sales, it remains the single largest category behind IPAs and “Seasonals”, with $254 million in sales. Given that Seasonals can be any style, and are brewed to capitalize on shorter annual trends, they should be considered separately, and Wits deserve recognition as “Prince” to IPA’s “King”.

Down the line, and skipping “Craft Variety”, which will typically consist of IPA offerings, or a mix of top selling styles, we find Golden Ale, down 7 percent for $184 million in sales for 2025. Rounding out the +$100 million sales club is “Craft Other Pale Lagers”, a bit of a catch-all. The theme of lighter brews dominating behind IPA continues.

Then we reach Craft Fruit/Veggie/Spiced, which, as another amorphous category, may not fully represent taste preferences. This could be Coffee Beer, Fruited Sours, or even Ghost Pepper Beer… Realistically of course, Fruit Beer will comprise the largest cross-section of this segment, and rightfully so. There’s always room to kick up a brew with fruit. Logically, if this can be done gently, subtly, with an eye towards refreshment, brewers may find success in enhancing a Golden Ale with a hint of fruit, like apricot, for example. The proof of concept for apricot, specifically, in Magic Hat #9 and Pyramid Apricot Hefeweizen, are a nostalgia well currently untapped.

Tapping Nostalgia in 2026

It bears repeating in 2026 that nostalgia is powerful when properly leveraged. After all, there’s a lot to be nostalgic about in the Age of Novelty, where beautiful things emerge and fade out in ever-increasingly fleeting fashion.

Craft beer is clearly not what it was a decade ago. Nor is our nation. Nor is the state of how we interact, which includes how we drink. People are longing for tangible connections to the past, because everything now is deleted, swiped right, passed on for the next fad. What spoke to you that still speaks to you? What experiences with a beer do you miss? What style of beer whisked you into the world of craft beer in the first place, and why? Exploring these questions may lead to wells of nostalgia that people would be willing to pay for. It could be a beer style. It could also be a beer which recalls an idea, or way of being. How can brewers bring the past into the timeless present in the coming year?

Top 100 Beverage Brands in 2025

Modelo Especial, for another year, is beer’s top brand. $3.6 billion in dollar sales. Nearly 10 percent of market share among the Top 100. The point doesn’t need belaboring. This is a beer that uniquely appeals to all. Flavorful, refreshing, crushable, and classy. Imported, and especially appealing to the Hispanic population which drives its sales. We’ve said it for years now and this point does bear repeating: At well over 20 percent of the population beer needs to recognize this demographic and cater to it.

Corona, Dos Equis, Pacifico, Cheladas… A significant chunk of total beer sales is Mexican beer, or styles which are driven by sales to Hispanics. Craft beer historically appeals most to white males, who are now aging out as viable drivers of sales. Many of the above brands saw significant sales increases this year, which incidentally is likely a key reason why Modelo sold less. Victoria Lager, for example, grew 34 percent in 2025, vastly more than any other comparable brand. Consider demographics, and tailor accordingly. Mexican beer styles are the most reliable sellers, and well within reach of any craft brewer.

And a token reminder… The top five Chelada brands account for around $600 million in sales… How much thought does the average craft brewer give to this style of beverage? Start your own craft chelada brand, name it Chill-ada or Chill-ade, and you’ve tapped into an uncrowded billion dollar industry. All you’ve got to do is educate, or brand properly.

Michelob Ultra: King of Functional Beer

Michelob Ultra is the pioneering functional beer, and paved the way for much of the success NA beer is now enjoying. It’s considered generally healthy to have after running a marathon. It’s as low-cal and yet still enjoyable to drink as any beer can be. The branding is well-established, and sleek. All these reasons contribute to its vaunted position as the only other beer topping $3 billion in sales, and further, unlike Modelo Especial, Michelob Ultra saw a 4.3 percent sales increase in 2025. It now totals more than 8 percent of total dollar share for the Top 100 brands. Factor in Michelob Ultra Pure Gold and Lime Cactus, and you’ve got another few hundred million dollars going towards the same brand family.

As one of the few guaranteed growth areas for beer, how can brewers capitalize on functional beer? Try going beyond a light lager. Repurpose Table Beer as the ultimate performance related alcoholic drink and you may have a goldmine on your hands.

Another Functional Mode

It’s no secret that Seltzer is the favorite of all who despise bloating, calories, or simply the overload that comes with strong craft beer. While Seltzer is down 5 percent in total sales, it still boasts a $2.5 billion market, and a significant chunk of its sales decrease is simply leveling off, and losing share to the functional boom (plus premixed cocktails).

White Claw dominates among Seltzers, with infinite varieties and variety packs, many of which crack the Top 100 for sales. If you added them all together, they’d be well north of $1 billion, and probably closer to $2 billion. Their closest competitor, Truly Sparkling Seltzer, which boasts a few brands in the Top 100, might account for 1/10th of White Claw’s sales. You could almost consider it a monopoly.

While White Claw has always held the upper hand, its grip is tightening. We know Seltzer is here to stay. Therefore, for brewers hoping to make inroads on this lucrative front, use White Claw as a benchmark, and either aim to nail what that brand does best, or try something different.

Different might look like more exotic flavors, rather than the core of varying fruit and berry flavors. La Croix might be a good example, as it has established a wider line of interesting “essences” for flavoring. Cherry Blossom, Mint and Lime, Beach Plum, or even the obscure, yet sunny “Sunshine”. Note, for the last, it’s appealing to an entire concept, rather than an exact flavor. There may be a place for seltzer lines that attempt to encapsulate those intangible feelings or experiences.

Rogue Waves Goodbye, Among Others

Rogue has gone bankrupt. Pike Brewing announced the closure of its iconic Pike Place Pub. How many other legacy brands have gone by the wayside? It’s a year of consolidation, bankruptcy, closure, merger, and perhaps, for a small brewer with an eye for steady focus on their community, without the need for drastic expansion… survival. Survival comes from doing the little things right, like serving beer in matching glassware.

Sidenote: You may be able to snatch up high quality brewing equipment, or even unopened kegs when a brewery liquidates. One brewer was recently selling full kegs with drinkable beer for $25. Stainless steel from a keg can be recycled for up to $100.

A Tribute To The Insanity

The halcyon days of starry eyed craft drinking are gone… for now. It was, to a degree, inevitable. Bell bottoms had to go out of style in order to have a resurgence. Yet, for all the horrifying Franken-brews, there was a glimmer of something innocent, truly exciting going on when beers like Rogue’s Voodoo Donut Bacon Maple Ale was concocted. Or Rogue Beard Beer, brewed with yeast cultured from the head brewer’s beard, which was apparently not that bad tasting.

Wynkoop Brewing made a stirring contribution with its Rocky Mountain Oyster Stout, brewed with real bull testes, while Icelandic Brewery Stedji brought us Hvalur, which tempered its pure glacial water base with whale testicles smoked in sheep dung. There was Mamma Mia! Pizza Beer, Cave Creek Chili Beer, which came with a real chili pepper in the bottle, Martin House’s Fiery Crunchy Cheesie Bois Flamin’ Hot Cheeto simulacra, and Evil Twin Spicy Nachos, brewed to taste like, you guessed it…

Some actually were good, though a bit out on a limb. Kaffir lime, coconut and curry spice offerings from New Belgium and Ballast Point were totally out of left field, but complex and enjoyable. There seems to be a clear leader for the most absurd, poor taste, worst judgment beer of all time, however, and it’s not the 67% ABV “Snake Venom” ale from Brewmeister.

That dubious honor goes to “The Order of Yoni”, which specializes in brewing beers with lactobacillus cultured from the nether-regions of Slavic models. Choose from two different blondes or a brunette (after all, these beers are categorized foremost by the model’s hair type) and savor a special beer which starts like this:

“The gynaecologist collects a vaginal smear from the models. These smears are taken to a laboratory where bacteria are isolated, cleaned, then analysed and multiplied. At the end of the process, the bacteria are used to produce the pure lactic acid that goes into Yoni beer.”

That’s not the profoundly human element we’re looking for in our beer. So, in a way, there are upsides to the changing beer landscape. These marketing ploys were never reliant on time-tested quality, and could never sustain themselves as legacy brands. They were formed in the first nanoseconds of brewing’s big bang, and faded into the aether to make way for the long burning stars which may not burn brightest, but supply a consistent source of light.

The Upside of a Downturn

What makes beer so great is also what is limiting sales. The best beers are meant to savor, reflect upon, share. They do not need to be overstated and flashy. Imagine a Mr. Beast beer, or any other godforsaken influencer beer. It would feel, to the connoisseur, like heresy, losing the forest for a gaudy tree.

Connoisseurs are “critics in matters of taste.” The critic engages critical thinking, which engages the prefrontal cortex. The critic must operate from a state of relaxation, in order to fully access the senses and transfer that sensory information to the “higher brain”, to fully describe what they are experiencing.

Mr. Beast does not want you to slow down, engage your senses, or make thoughtful choices based on a variety of subtleties. He wants to overwhelm your reptile brain with chocolate, greasy hamburgers, light and sound.

If the craft beer industry can’t rely on light and sound to trump up numbers, maybe brewers will rely more heavily on time tested quality assurance. The spirit of the nanobrewery is infectious, yet sometimes, the beer tasted a bit infected too.

If we can slow down, accepting that beer is not in its Jay Gatsby era, we might be able to finally fully appreciate what really matters: quality beer for a quality drinking experience in the presence of quality company. That’s all we need. Nothing more.

A Note On The Numbers:

Our numbers come primarily from Circana’s 2025 Total US Multi-Outlet + Convenience Beer Data, which offers a comprehensive cross-section of sales by category, style, brand and more. This data, combined with a survey of consumers, forms a unique platform for speculation on annual trends.

Comments 0

No Readers' Pick yet.